The staggering financial toll of family caregiving

- Select a language for the TTS:

- UK English Female

- UK English Male

- US English Female

- US English Male

- Australian Female

- Australian Male

- Language selected: (auto detect) - EN

Play all audios:

“America’s family caregivers put family first, helping their parents, spouses and others stay at home,” said Nancy LeaMond, AARP Executive Vice President and Chief Advocacy & Engagement

Officer. “They spend thousands of dollars every year on this care, while juggling work and family responsibilities. We urge Congress to put money back into the pockets of hardworking family

caregivers by passing the Credit for Caring tax credit.” MAKING SACRIFICES When Maylia Tsen took on the role of family caregiver for her parents, one thing quickly became apparent: She

wouldn’t be able to simultaneously keep up with the demands of her career (she’s held high-level sales/marketing positions at Pepsi-Cola, Bausch & Lomb and Sprint); the business travel,

alone, made her schedule unpredictable from one week to the next. Thinking she could draw on her years of experience and generate a comparable income — with the added bonus of working

flexible hours — she left the corporate world around 2005. She struck out on her own right around the time her parents relocated from New York to Laguna Nigel, California, to live near her.

More than 25 years later, she’s still caring for her now 97-year-old father (her mother died of complications from Parkinson’s in 2014), and making around 10 percent of the six-figure salary

she once earned. “I’ve given up a lot,” says Tsen, who works part-time as an online tutor and occasional business consultant. “All the struggles and challenges in juggling to make ends

meet have been tough. I have short windows of maybe an hour or two for myself, but unless you can afford a caregiver, which is very costly, you pretty much have to be with (your loved one)

all the time. I wear at least five hats at any given time.” Tsen is typically up at 7 every morning and, over the course of a typical day, helps her dad dress, provides meals, takes him to

appointments and tends to his medical needs, including helping care for his diabetes-related wounds. Maylia Tsen has been a caregiver for her father for 25 years. They recently celebrated

the Lunar New Year together. Courtesy of Maylia Tsen Arguably the worst part: “I’ve gone through all my savings, retirement, everything,” she says. “I have to continue to work; there’s no

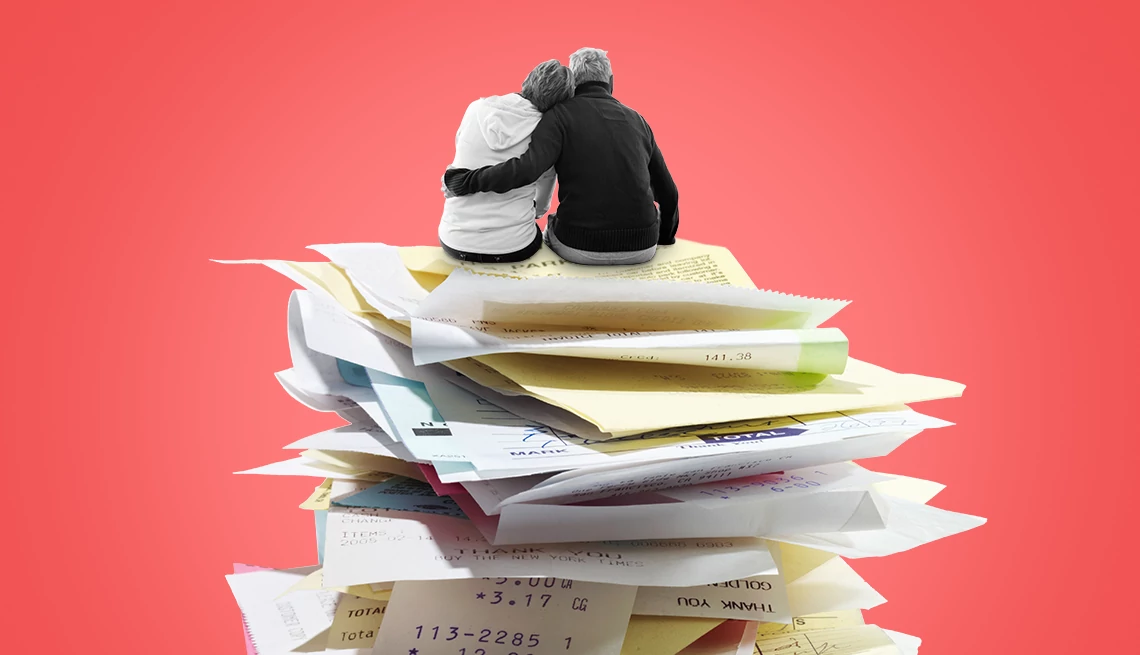

way for me to retire.” Tsen’s experience is far from unusual. According to a 2021 AARP report, nearly half of all family caregivers in the U.S. have experienced at least one financial

setback — among the most common, dipping into their savings — due to caregiving and around one in five had to cut back on their health care spending or reduce the amount they save for

retirement. STRUGGLING TO REBOUND On average, caregivers spend 26 percent of their personal income on caregiving expenses. One in three dips into their personal savings, like bank accounts,

to cover costs, and 12 percent take out a loan or borrow from family or friends. Some, like Amy Goyer, run up credit card debt to meet the financial demands of caregiving. After more than a

decade of caring for her father, who had Alzheimer’s, and her mother, who had a stroke, Goyer was saddled with high-interest credit card debt. On the advice of bankruptcy attorneys and

financial advisors, she ended up filing for bankruptcy in 2019, a year after her father died. Now 64, she’s still trying to rebound financially, heading toward her retirement years with no

savings. “When you’re in your late 40s and 50s, you should be focused on saving for retirement,” says Goyer, AARP’s national family and caregiving expert. “I couldn’t do that. So now I’m

working with a financial advisor to figure out if I can ever retire.”